[ad_1]

A major tale in excess of the earlier two decades has been the rise in house price ranges. There are a lot of variables at enjoy. Restricted supply is a person. An inflow of people today moving to extra attractive locations is an additional. But rising desire charges are threatening to stymie the housing industry. There are even fears that some of the recent gains could be reversed.

That has pushed home enhancement retailers Home Depot (Hd 2.19%) and Lowe’s (Low 1.20%) very well down below the highs they reached at the conclude of last year. But all those fears may perhaps be offering buyers an prospect. Is 1 of them improved than the other? Wall Street thinks so. And these charts exhibit why.

Impression source: Getty Visuals.

One is often more pricey than the other

For the past decade, Wall Road has been ready to fork out a bigger valuation for Home Depot than for Lowe’s. As the valuation of the total inventory market place oscillated, the two house improvement stores did a dance of amazing predictability. Resembling poles of two magnets repelling just about every other, the price-to-revenue ratios held their length.

Hd PS Ratio data by YCharts

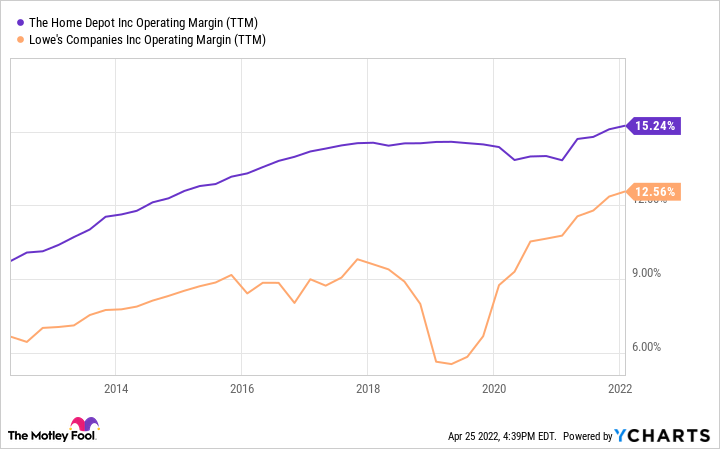

It is really also continuously extra rewarding

A person good rationalization is Household Depot’s profitability. Over that ten years, its operating margin stayed at the very least a person-fifth greater than that of Lowe’s. The company recently warned that profit margins would undergo as expenditures surge.

Administration went so significantly as to constitution its very own cargo ship to prevent the snarled world-wide offer chain. Historically, Lowe’s has used far more on bills like profits, promoting, and administrative features these kinds of as human resources and accounting. In 2021, the distinction was about a minor more than 2% of gross sales — around the hole in functioning margin.

Hd Operating Margin (TTM) details by YCharts

In sharp distinction to record, the current update at Lowe’s was optimistic. In February it elevated its comprehensive-12 months estimates for revenue and profits.

And it’s in a far better place to handle its personal debt

One area the place Lowe’s looks a lot more beautiful is the volume of credit card debt it carries when compared to Dwelling Depot. It has $30 billion in combined brief- and lengthy-expression debt on its balance sheet. Dwelling Depot has $45 billion.

But digging a very little further reveals that Household Depot is in a stronger economical situation, due to the fact it generates virtually 2 times the earnings before interest and taxes (EBIT). That indicates its occasions interest gained ratio — the selection of occasions the EBIT can go over annual desire payments — is substantially increased.

Small Moments Curiosity Attained (TTM) data by YCharts

It has grown more quickly, as well

All of this neglects the a single metric quite a few investors prioritize over all other individuals: development. In this article way too, Household Depot wins. Neither enterprise is in hypergrowth manner, and the two benefited a ton through the pandemic from consumers’ willingness to devote on housing. But more than the previous five- and 10-12 months periods, the prime line at Loew’s has expanded at a slower rate.

High definition Profits (TTM) details by YCharts

Which a single pays you much more to possess shares?

Investors might expect Lowe’s to make up for these perceived shortfalls by paying out a better dividend to shareholders. They would be erroneous. House Depot’s distribution far exceeds that of Lowe’s. It has for most of the past 10 years.

High definition Dividend Produce knowledge by YCharts

That doesn’t account for all of the methods to return capital to shareholders. Lowe’s has performed substantially a lot more stock buybacks in the previous number of many years. In reality, it has repurchased 17% of shares outstanding in just the earlier a few years. Property Depot has bought back just 6%.

Lowe’s also has extra area to enhance the dividend in the potential. It sends fewer than one particular-quarter of gains again to shareholders as dividends. For Home Depot, the number is about 4-fifths. Nevertheless, both of those can effortlessly do it for the foreseeable long term.

Is the altering of the guard near?

If you’re wanting to incorporate one of the major-box residence enhancement retailers to your portfolio, the historical metrics make a powerful situation for Property Depot about Lowe’s. But that could be changing. Differing 2022 outlooks and an intense buyback plan have Lowe’s hunting and sounding like the aged House Depot that Wall Avenue fell in enjoy with.

Both give traders publicity to an market at the heart of the American financial system. With solid funds return courses, sound margins, and manageable financial debt, there is no improper selection. But Dwelling Depot has proved it can execute over time. That is why I would lean towards it if compelled to decide on. Of program, you can find no rule versus obtaining each.

[ad_2]

Supply website link